SCORE JUNCTION

Turn Your Credit Score Into a Stronger Financial Advantage

Smart, structured credit improvement designed to help you qualify for better opportunities—without the confusion.

No hype. No shortcuts. Just proven credit-building strategies tailored to your situation.

Our Services

Who is ScoreJunction?

At Score Junction, we specialize in credit education, credit restoration, and document preparation services designed to help you take control of your financial future.

We guide clients through the credit repair process step-by-step, helping them understand their rights and take action to improve their credit profile—without the confusion or costly mistakes.

Credit Audit & Analysis (All 3 Bureaus)

Custom Dispute Strategies & Letters

Negative Item Disputes & Corrections

Credit Education & Score Improvement Guidance

24/7 Client Portal Access & Progress Tracking

Ongoing Support from a Dedicated Case Advisor

About Us

ScoreJunction was built on a simple idea: people deserve clarity and structure when it comes to improving their credit.

Too many services rely on vague promises or one-size-fits-all approaches.

We focus on strategy, education, and execution—so you actually understand what’s changing and why.

Mission

Our mission is to turn confusion into control.

We help individuals:-

1. Understand their credit profile

2. Take strategic action

3. Build sustainable financial confidence

Approach

What makes ScoreJunction different

We’re not here to promise unrealistic results.

We’re here to help you make smarter credit decisions—and see real progress over time.

Strategy-first, not guesswork

Focus on long-term credit strength—not quick fixes

Structured dispute processes

Clear communication every step of the way

If your credit is holding you back, you’re not alone.

Most people don’t have a clear plan—they’re guessing.

Getting denied or offered high interest rates

Old negative items dragging your score down

Not knowing what actually works anymore

Ready to get started?

ScoreJunction gives you a clear path forward.

We combine credit analysis, dispute strategy, and profile optimization to help you improve your credit with purpose.

Identify what’s hurting your score

Take action with structured dispute processes

Build positive credit that lasts

Ready to get started?

Kathy – Plano, TX

I am extremely happy with the results Lesley produced on my behalf in regards to my credit reports. I had tried to deal with the credit reporting agencies on my own, and I was not able to achieve any sort of change or results in my credit. After hiring Score Junction, she achieved my credit goals in a matter of months and produced the results I desired but couldn’t achieve on my own.

Thank you so much!

Cindy , Midland, TX

I am a single divorced parent. My husband left me quite alot of debt and my credit was very bad. I have been with Score Junction for 4 months now and my credit score went from 490 to 675. The Credit Bureaus lied to me when they told me no one can repair credit.

Thank you Lesley.

Ken - Red Oak, TX

I was tired of being declined loans due to my old past mistakes, then Score Junction came to the rescue! They removed the outdated information, updated several accounts, and deleted several other negative entries. They helped me understand why I was in the situation I was in and what to do to keep from going there again. Thanks Lesley!”

CREDIT TOOLS

To enroll in our services, we require credit monitoring for analyzing and tracking your credit scores and profile updates. Please order below

Jump-start your credit rebuilding with secure cards that require no credit check. Avoid adding new inquiries that can lower your score while building positive credit history and strengthening your profile for better score growth.

get started

Not just credit repair—credit positioning.

We don’t just aim to remove negatives.

We help you position your credit profile for approvals, limits, and long-term leverage.

get started

Not just credit repair—credit positioning.

lorem ipsum Quam est faucibus porttitor luctus sem phasellus. Pretium neque aliquet .

STILL NOT SURE?

Frequently Asked Questions(FAQs)

Common Questions

What is a Credit Score?

A credit score is a number generated by a mathematical formula that is meant to predict credit worthiness. Credit scores range from 300-850. The higher your score is, the more likely you are to get a loan. The lower your score is, the less likely you are to get a loan. If you have a low credit score and you do manage to get approved for credit then your interest rate will be much higher than someone who had a good credit score and borrowed money. Therefore, having a high credit score can save many thousands of dollars over the life of your mortgage, auto loan, or credit card.

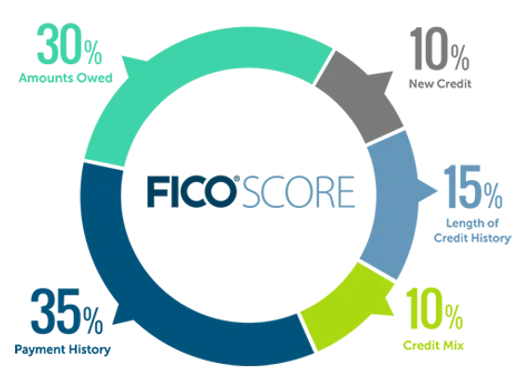

What affects your Credit Score?

35% – Payment History

30% – Debt Ratio

15% – Length of Credit History

10% – Types of Credit

10% – Number of Credit Inquiries

Will we help you to dispute negative items in your payment history?

- We will show you how to maximize your debt ratio score, even if paying off credit cards is not an option.

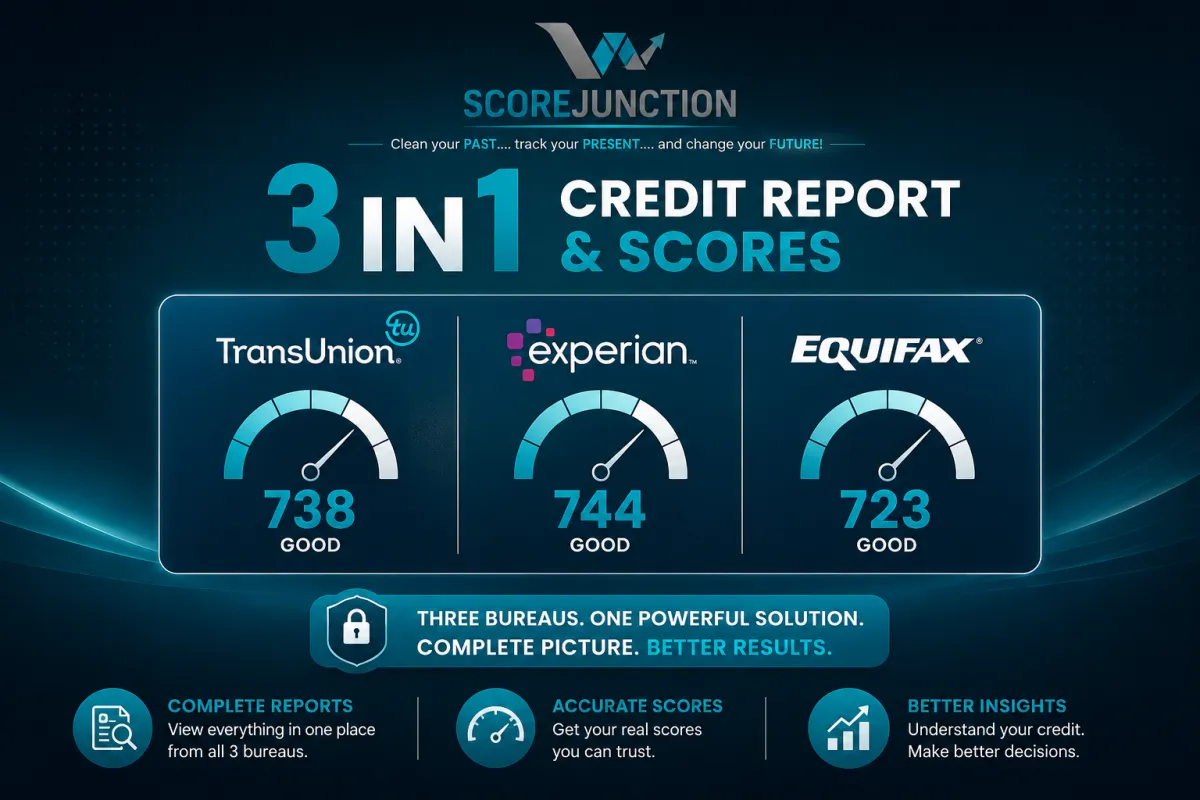

- We can also help you to removing credit inquiries from your credit report. Most people are aware of the three credit reporting bureaus, Equifax, Experian and TransUnion. The average difference in scores between the highest and lowest of your credit scores, from the three bureaus, is 60 points. This is the result of the credit bureaus having different items on their report, which may be correct, incorrect or are not reported in full compliance with credit law. According to a recent study, nearly 80% of all credit reports have serious errors on them and this does not even include the even smaller errors for which we look.

- If you cannot remove at least 25% of the negative credit items from all three of your credit reports, we will refund 100% of your fee.

What can I do to help raise my credit score?

- Pay all of your bills on time, every time. This includes your utility bills, mortgage and auto payments, and all of your revolving lines of credit like credit cards. Check your credit report at least once a year. You can find out how to challenge bad information on your credit report here.

- Never charge more than 30% of the available balance on any of your credit cards. Banks like to see a nice record of on-time payments, and several credit cards that are not maxed-out. If you are carrying high balances on your credit cards, then make paying them down below 30% a priority. Do use your credit cards – Many people who make mistakes with their credit believe that the best way to fix things is to never use credit again. If you are afraid that you cannot handle your credit cards correctly then the best policy is probably this one: Run only your utility bills on your credit cards each month, and then pay the balance in full by the due date. This ensures that your utility bills get paid on time automatically, and as long as you keep the habit of paying off your credit card balance each month your score will continue to go up. Leave the credit cards locked in a safe or drawer at home.

- Keep your accounts open as long as possible – Even if you are no longer charging on the card. The best policy is to keep those unused accounts open, blow the dust off your card every few months to make a small purchase, then pay it off. How long each of your accounts have been active is a major factor in your credit score.

- Remember that this all takes time – Following the above steps consistently over a long period of time will increase your credit score and allow you to qualify for better loans and lower interest rates. Repairing your credit score does not happen overnight, so if you do these things for a few months and do not see a large increase in your score, do not give up. They are all habits that you will want to maintain throughout your life, as they will help you to keep your finances and lines of credit under control.

How long will certain items remain on my credit file?

- Delinquencies (30- 180 days): A delinquency may remain on file for seven years; from the date of the initial missed payment.

- Collection Accounts: May remain seven years from the date of the initial missed payment that led to the collection (the original delinquency date). When a collection account is paid in full, it will be marked as a “paid collection” on the credit report.

- Charge-off Accounts: When a delinquent account is sent to a collections company. This will remain for seven years from the date of the initial missed payment that led to the charge-off (the original delinquency date), even if payments are later made on the charge-off account.

- Closed Accounts: Closed accounts are no longer available for further use and may or may not have a zero balance. Closed accounts with delinquencies remain for seven years from the date they are reported closed, whether closed by the creditor or by the consumer. However, the delinquency notation will be removed seven years after the delinquency occurred when pertaining to late payments. Positive closed accounts continue to be reported for ten years from the closing date.

- Lost Credit Card: If there are no delinquencies, credit cards reported as lost will continue to be listed for two years from the date the creditor is contacted. Delinquent payments that occurred before the card was lost are reported for seven years.

- Bankruptcy: Chapters 7, 11, and 12 will remain on one’s credit report for ten years from the filing date. A Chapter 13 bankruptcy is reported for seven years from the filing date. Accounts included in a bankruptcy will remain for seven years from the date reported as included in the bankruptcy

- Judgments: Remain seven years from the date filed.

- City, County, State, and Federal Tax Liens: Unpaid tax liens remain for fifteen years from the filing date. A paid tax lien will remain on one’s score for 10 years from the date of payment.

- Inquiries: Most inquiries listed on one’s credit report will remain for two years. All inquiries must remain for a minimum of one year from the date the inquiry was made. Some inquiries, such as employment or pre-approved offers of credit, will show only on a personal credit report pulled by you.

What Information cannot be in a credit report?

- Medical information (unless you provide consent)

- Notice of bankruptcy (Chapter 11) more than ten years old

- Debts (including delinquent child support payments) more than seven years old

- Age, marital status, or race (if requested from a current or prospective employer)

Refund Policy

You are entitled to a 100% refund on all monthly payments if:

1. We do not remove any negatives worked on.- You have had 120 days (4 consecutive months) from the time that you retain our services.

2. You have not used a credit-consulting agency nor attempted to repair your own credit at least 1 year prior to signing up for our services.

3. You have had no new collections or missed payments during the time frame we are assisting you.

4. You have maintained credit monitoring services at all times during the time frame we are assisting you.

5. You agree & have sent updated reports/responses from the three credit bureaus & creditors to us within 5 days of receipt.You should receive updated credit reports every 35-45 days and make us aware if updated reports have not been received.

Clean your PAST... Track your PRESENT... and Change your FUTURE

Email: [email protected]

Phone: (214)-449-8804

quick links

Business hours

monday: 8am - 5pm

tuesday: 8am - 5pm

wednesday: 8am - 5pm

thursday: 8am - 5pm

friday: 8am - 5pm

Copyright 2026. Dallas, Texas. All rights reserved.

Facebook

Instagram

TikTok